Definitely a trend I see around me (Europe, 30 years old).

All of my friends able to buy got at least 30k - 50k from their parents.

Is it the same around you? How do you deal with this?

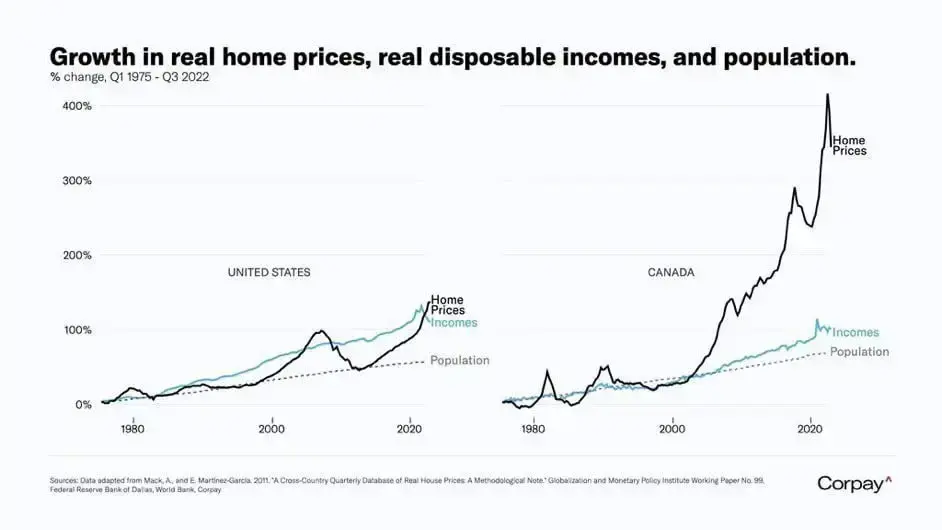

Also, some data from a few days back:

https://discuss.tchncs.de/post/2426785?scrollToComments=true

Well I mean yeah we bought our house off my father-in-law who sold it at extreme mates rates, and my parents paid my half of the deposit. And I don’t think that’s news, that’s the way it’s been for people I know for the last 10 years or so. We only relatively recently managed to get a mortgage because I was doing contract work for a long time which paid a lot better but isn’t stable enough to get one.

I feel lucky because I know there’s no way I’d be able to live in our own house without parental help - we’re both public sector workers so we do alright but don’t have any money to put aside for savings. Which also means we won’t be able to return the favour for our son, or at least not to the same degree. I’ve just turned 40, I have friends a few years younger who are working but still live with family because they have no other realistic option.

My father-in-law worked in the property world as a surveyor since the 70s or so and when his father died young he bought some flats in London with the inheritance. His dad was a miner so the flats were dirt cheap but they were in King’s Cross which back then was known for drugs and prostitution. He despised the 80s, because he knew it was short term gain for his generation at the expense at the next ones - instead of investing in the future, governments were just selling everything off to the private sector for short term gain, and so he had this masterplan of saving all this stuff up for his kids. He’s an interesting person to talk to.

My parents had enough money to put aside in savings for the future for me and my sister every month, which went towards the house deposit and my university fees. They didn’t own any flats in London but they had that extra to put aside. That’s what our generation doesn’t have, the ability to put anything significant aside for the future - it all goes on bills.